Payments

How To Find the Best Payment Management System

Find out how to choose the best payment management system for your business. Book a demo with Spenmo today.

Payment apps make it easier for small businesses to manage their payables in an easy and timely manner. Check out these payment apps for your business!

Imagine buying materials from your suppliers and paying through cash alone. You may end up seeing piles of invoices on your table, losing track of your payables, or worse, not having enough cash available.

Many businesses, particularly the small-scale ones, rely on cash or cheque payments. But, in a fast-paced market, efficiency is a primary contributor to success. Now that we are still in the pandemic, physical transactions can be inconvenient. Worse, some vendors are apprehensive about accepting cash payments.

Cashless transactions are vital to businesses today. Whatever your business is, there can be unexpected expenses. It is good that virtual credit cards (VCCs) and digital wallets can help you do business anytime you want. This article will take a closer look at some popular payment apps for small businesses.

Long before the pandemic started, cashless transactions were already booming in the ASEAN region. Businesses and consumers shifted from cash to credit cards and payment apps. In 2013, Singapore was one of the leading countries to adapt to this trend. Its shift to a cashless society became more evident.

For instance, cards and e-payment comprised 69% of consumer spending, 1% shy of South Korea. The global average percentage was only 66%. For the next three years, Singapore slowed down compared to other city-states in Asia. In a 2015 study commissioned by the MAS, cash transactions rebounded to 60%. This increase came from wet markets and small shops, comprising 80%.

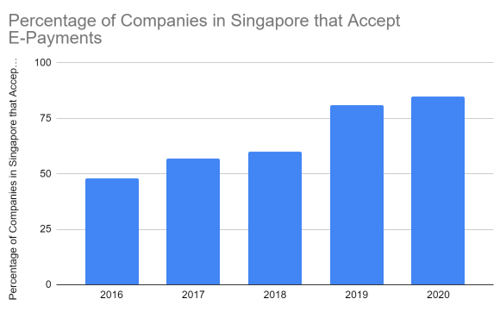

Yet, e-payment became a popular trend again in 2017-2019. It revolutionised and dominated payment systems globally. In the same year, Spenmo emerged and took part in the e-payment revolution. Its timing was perfect as more businesses adopted this payment system. From 48% in 2016, e-payments rose to 81% in 2019.

Meanwhile, it took quite a long time to catch up with the changing market. It was the second-largest cash-based economy in 2017. It is easy to understand why. Sixty-four percent of its population are unbanked, while 96% of adults do not have credit cards.

But since 2019, it has appeared that cash domination would not persist for an extended period. More Indonesians have shifted to cards and payment apps. E-wallets have become a popular cashless payment method. Since then, it has dominated the fintech industry, with 54.6% of cashless transactions.

The number of payment app users grew by more than four times, exceeding 2 billion. It was no wonder that payment apps became a popular trend for small businesses.

The pandemic drove the drastic rise in digital payments. It caused a domino effect as most businesses opted to shut down. E-commerce became a favourite, given the limited operations and restrictions. The best payment apps for small businesses were integral for recovery and growth.

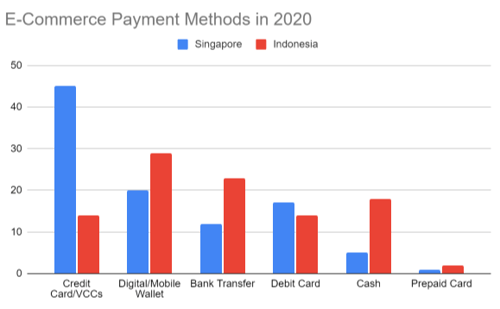

Singapore had the most visible acceleration towards it. During 1Q 2020, about 100,000 Singaporeans did online spending for the first time. It was due to the 44% growth in online grocery shopping. Digital payments on e-commerce and food deliveries grew by 36% and 40%. The percentage of businesses accepting e-payments increased to 85% during the second half.

Taken from Statista

Contactless debit and credit cards remained the top choice. Keep in mind that contactless cards differ from the typical debit and credit cards. You don’t have to swipe them at the billing counter. You only have to wave or tap them on the contactless terminal without entering your pin. VCCs are another favourite since Singaporeans can pay even without their physical cards.

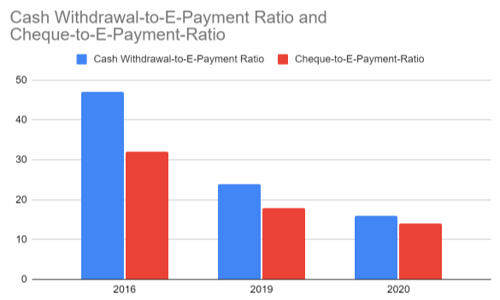

Meanwhile, digital payment apps emerged as their third choice, with Paypal and GrabPay as the top pick. You can wave your phone at the counter to pay like contactless cards. It led to a decrease in the cheque-to-e-payment volume to 12%. The cash-to-digital payment ratio fell to 17%. The estimated percentage of cash transactions was 39%, but the actual value was even lower at 37% only. Despite this, Singapore does not intend to be a 100% cashless society, at least in 2021-2025.

Taken from The Strait Times

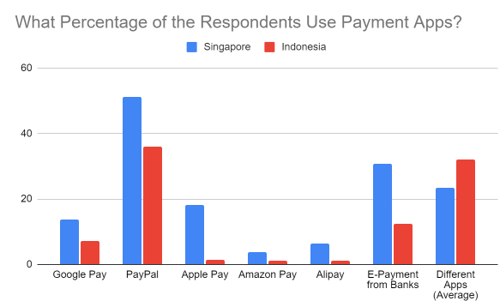

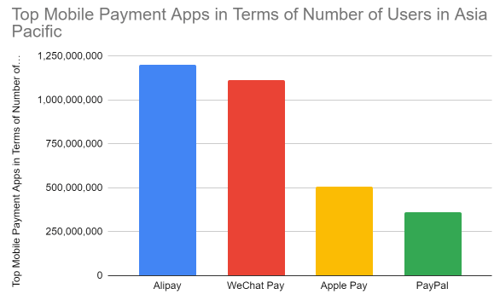

Another survey conducted earlier this year confirmed the findings in 2020. Among the surveyed individuals, 66% used cashless payment methods. Meanwhile, 78% said they would shift to digital payment apps after the pandemic. Now, contactless and online credit cards are still the number one option. But, digital payments are becoming more popular and starting to overtake card transactions. It extends to its neighbouring countries and Oceania. In fact, 46% of 1.8 billion people in the Asia Pacific use e-payment apps daily.

Meanwhile, Indonesia has room for improvement as bank penetration is only 48%. But, more people, even the unbanked, started to embrace the use of e-payment apps. Digital payments grew by 38.6% and reached $13.95 billion. With that, local fintech players like GoJek and Dana have dominated Indonesia. Other apps like Paypal are keeping up with the competition. As projected, e-money transactions will increase to $18.47 billion.

Taken from Statista

Taken from Statista

Given all these trends, studies project a further increase in e-wallet users in 2025. In a survey, 74% of business owners in Southeast Asia are now open to cashless payments. The percentage was even higher in Singapore at over 80%. Moreso, 49% of the commercial bank customers in urban areas have digital payment apps. Hence, studies estimate that 84% of the population will have access to e-payments apps in 2025.

Taken from TECHWIRE ASIA

Regardless of the business size, the need for payment apps has become more visible. Efficiency in the fast-paced world is a factor in success. Payment apps save more time and costs than you think.

Consumers now rely on these more than ever, given earlier data. Since your customers and suppliers use digital payment apps, you have to catch up. Here are some reasons why mobile payment apps for small businesses are vital.

Now that we are still facing the threat of the pandemic, people still tend to avoid physical contact. For instance, you run out of supplies, and you have to rush products. You cannot always ask your vendors to deliver right away, especially if you are still a newcomer. Chances are, you will go to stores to buy right away.

With payment apps or virtual cards, You do not have to queue up to the bank to make a deposit or issue cheques. They help you reduce the transmission risks in your business. Moreso, many consumers are now on the internet. Even your suppliers may be there. Since the boom of e-commerce, intensified by the pandemic impact, transactions went online. With that, you can also order supplies and pay online.

Given the previous point, digital payment apps improve customer experience. Card and digital payments apps offer flexible payment methods. These enable your customers to pay anytime and anywhere they want. Also, it makes the checkout process faster.

They can shop with only their phones at hand. They do not have to worry about risks associated with lost cash and cards. Now, these are more crucial as customers value convenience and safety more. It will pay off as you establish brand loyalty and attract more customers.

With digital payment apps, you can make in-store purchases with your cellphone alone. Thanks to Near-Field Communication (NFC), you can shop even without cash or cards. You can wave your mobile phone at the counter and add a PIN or fingerprint password to your phone and payment app for better security.

These use protected code or encryption against personal data threats. The actual number of your card is not stored on the device and the retailer. Like VCCs, it assigns temporary numbers for each transaction. In that way, hackers will not get access to your data or devices. In short, payment apps provide extra layers of security to your financial data.

The recent data presents the number of consumers and businesses with payment apps. With more people adapting to cashless transactions, you should keep up with the trend. Chances are, many stores will prefer cashless payments and refuse you. Perhaps you do not know much about it.

Even in the western part of the world, cash spending dropped. In the US, for example, 28% of people stopped using money since the pandemic started. More than 50% of the respondents tried to avoid in-person transactions in a recent survey. In fact, 7% added that merchants refused to accept payment if paid in cash.

South Korea and China had the same analysis. In Singapore, the expected cash transactions in 2020 were 39%. However, due to fear and restrictions, cash transactions went down to 37% only. Contactless cards and digital payment apps have become a staple. As such, you have to be more open to digital payment apps. Let’s admit that the new normal is speeding up the changes in the payment system.

Aside from convenience and security, payment apps provide valuable management tools. They help in bookkeeping and tracking transactions. They generate invoices or receipts shared via email. Given this, you do not have to worry about dealing with piles of invoices on your table.

Even more, mobile payment apps help you track customer trends and inventories. They allow you to understand customer demands better. You can check which products and services have more potential. Hence, you can improve them and your services to increase revenues.

Our reliance on cash has diminished, especially in the last year. The e-commerce industry has fueled our need for convenient payment systems. Thanks to payment apps, businesses and consumers can purchase goods and services using their phones without sacrificing security.

More so, it improves customer experience and establishes brand loyalty. Small business owners must consider adding payment apps as payment options. If you wish to have one, reach out and seek assistance from Spenmo. It provides quality fintech products and services for businesses.

Find out how to choose the best payment management system for your business. Book a demo with Spenmo today.

Expense management system helps businesses automate the recording, tracking, approval and payment with the use of an expense report software.

Technology has paved the way for a better, faster, and more convenient payment process. Here are some ways payment automation can drive business...